We're committed to strengthening our communities. See how we're making an impact.

We learn what matters most by asking you one simple question: What would you like the power to do?

Proud supporter of every goal

Teaming up to support achievements in the game of soccer, and across our community.

No matter what your financial goals are, we’re here to help

1 of 2

We’re helping support communities impacted by the wildfires

In the wake of the devastating Palisades, Eaton and other wildfires that swept through Los Angeles County and beyond, Bank of America has taken a lead role in coordinating financial relief and reconstruction efforts.

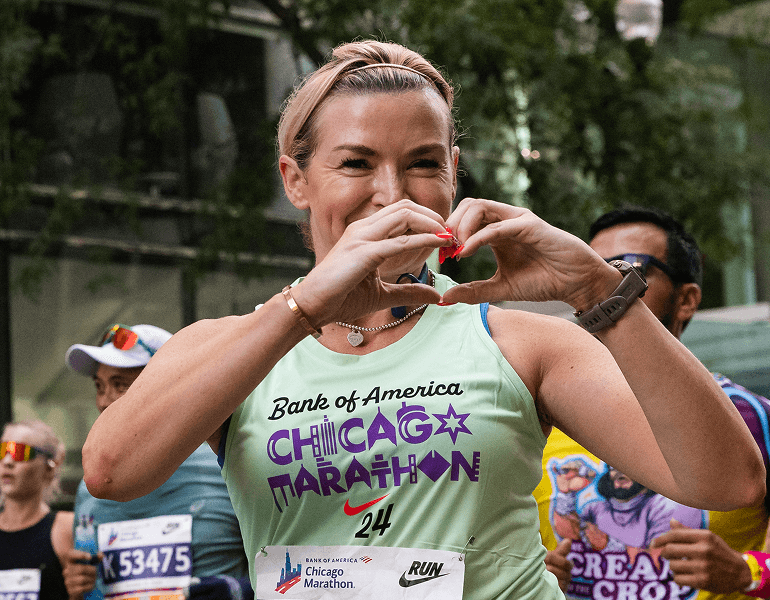

More than a race

See how the Bank of America Chicago Marathon drives positive economic change in our latest impact report. In 2024, this event helped raise millions for charities, supported over 4,500 jobs and more.

2024 Bank of America Annual Report

See how our commitment to Responsible Growth has continued to fuel our company's success.

Helping clients achieve their financial goals

For four years in a row, J.D. Power has certified Bank of America for Outstanding Customer Satisfaction with Financial Health Support – Banking & Payments. ***

Pursuing and enabling the dreams of entrepreneurs

Entrepreneurs enhance the character of cities and towns across our country. Take the founder behind Isla Veterinary Boutique Hospital. Dr. Josh Sanabria started his own veterinary hospital in Dallas, Texas – and we've supported his endeavors from day one.

Owner Josh is just one of the three million small business owners that we work with every year, helping them realize their potential.

Hero image: Natalie J., Financial Center Market Manager

*** J.D. Power 2025 Financial Health Support CertificationSM is based on exceeding customer experience benchmarks using client surveys and a best practices verification. For more information, visit www.jdpower.com/awards