At Bank of America, we’re committed to helping make financial lives better through the power of every connection. Learn how we’re empowering our clients, employees and communities to achieve new possibilities.

Keeping you moving toward your goals — big or small

What would you like the power to do?®

Making an impact in ways that matter

Making way for FIFA World Cup 2026™

As the official Bank of FIFA World Cup 2026™, we are committed to helping our clients, supporting communities and forging legacies. With our investment in soccer, we can drive bigger impact and opportunities. Bank of America champions everyone who dares to ask – What would you like the power to do?®

Celebrating America’s 250th anniversary

As the United States of America approaches its 250th anniversary, Bank of America is proud to celebrate. We also reflect on our role in driving meaningful impact across businesses and communities throughout key moments in history.

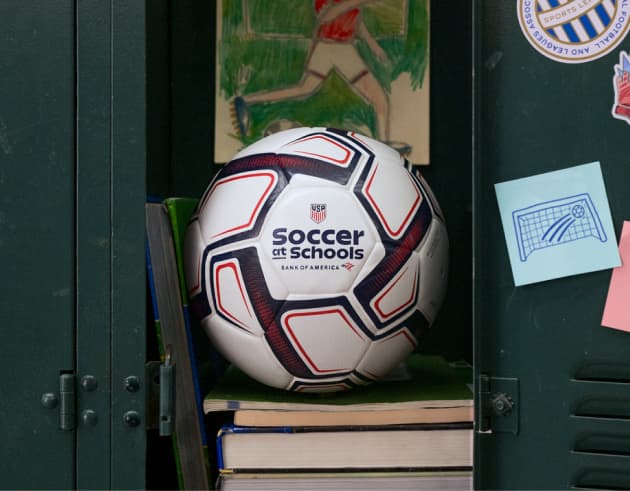

Soccer is in Session

Bank of America and U.S. Soccer are committed to helping bring the game and its lessons to schools across the nation.

Turn possibilities into achievements

Helping individuals, companies, communities and employees achieve their goals.

Leading through mentoring

A retired U.S. military leader with 30 years of service, John Milsap now serves as a Human Resources Manager at BofA – focused on coaching, mentoring and developing emerging leaders. Bank of America is proud to support his professional growth and share his journey.

Supporting economic mobility

Creating access to livable-wage jobs helps individuals improve their financial lives and promotes a thriving economy for our business to succeed. Helping people obtain stable employment is one way Bank of America supports economic mobility in communities.

Unlock kids’ potential

Sir David Beckham is one of the world’s most iconic figures. With success on and off the pitch, he asks how he can inspire others — because you never know where soccer’s next great talent is practicing.

Money confessions

Weighed down by money missteps? You’re not alone. Watch people share their experiences and get helpful guidance on overcoming money challenges from Better Money Habits® Champions.

Advance with my community

Jamal Fayyad’s entrepreneurial ambition and love for his community brought the Rio Grande Valley Red Crowns Soccer Club to life. Now, he's asking how he can inspire others to follow their dreams.

Local experts. Here for you.

Our teams are dedicated to helping people and businesses in communities across the country. Give back, build your savings or simply keep up with a changing economy with tools, resources and support from our local experts.

Learn more. Do more.